Diversification is No Free Lunch

Introduction

Over the last few decades, the lackluster performance of traditional active managers has fueled the rise of “closet indexing,” For some, this trend, and the related systemic underperformance of the active management industry, have renewed interest in concentrated investing in pursuit of improved investment performance. This paper leverages empirical evidence and expert insights to outline the merits of concentrated investing as an alternative or complement to more diversified solutions.

Diversification: A Brief Overview

In 1952, Modern Portfolio Theory (“MPT”) emerged as a landmark mathematical model that posited diversification as the key to reducing risk while simultaneously enhancing returns. Harry Markowitz, the Nobel laureate and architect of MPT thus declared that “Diversification is the only free lunch.” Unfortunately, as with most good things, MPT became overused and misapplied in practice, producing overly diversified portfolios. In our opinion, this over diversification has been the primary driver of systemic underperformance within the active management industry over the last few decades, as managers have become “closet indexers” whose portfolios closely resemble their benchmark.

Gresham has long preferred investing in portfolios concentrated in our managers’ best ideas. This approach arises from our frustration with the bland portfolios of traditional actively managed approaches. Fortunately, we have been able to find compelling investment solutions that run counter to this industry convention, which we believe may create excellent long-term results for our clients.

Active Share Defined

In 2006, a study from two professors at the Yale School of Management’s International Center for Finance introduced the term “active share” to measure the percentage of a portfolio that differs from its benchmark index.1 This study illuminated a problem within the U.S. mutual fund industry: Funds that are highly diversified (i.e., those with a low active share) tend to underperform compared to those with a high active share. This intuitively makes sense; many of the holdings in the portfolio are not performance oriented, but rather diversifying “filler” to enable better benchmark tracking. These overly diversified “benchmark-huggers” seemed to prioritize the interests of their parent firm (e.g., increase assets under management) rather than those of their investors (e.g., benchmark-relative performance). Further, their often high active management fees are charged on the entire portfolio, including the filler portion, implying an even higher effective fee rate for their active management, since only a portion of the portfolio is truly active (or different from the benchmark). For example, when a fund charges a 1% fee but only half the fund is actively managed, you’re effectively paying a 2% fee on the active portion since the other half is merely tracking an index, something you could achieve at very low cost.

The Waning Success of Traditional Active Managers

Over the past two decades, active fund managers, especially those with lower active share, have struggled to consistently outpace their designated benchmarks. Numerous industry reports highlight this issue:

- A report released by Morningstar in 2022 noted that over a ten-year period, approximately 80% of global large-cap blend mutual funds fell short of their respective benchmarks.2

- The same 2022 Morningstar study found that the decade-long success rate – a measure combining survival (fund remaining in business) and outperformance versus passive peers – hovered around a paltry 25%, and only 10% for U.S. large cap funds.3

- A 2023 report from S&P Dow Jones Indices revealed that over a span of 15 years, roughly 85% of actively managed international mutual funds underperformed the S&P International 700 index, a broad proxy for developed international equity markets.3 Moreover, this report revealed that over the same period, an alarming 90% of emerging market mutual funds underperformed their respective benchmarks.4

While it might seem safer for active managers to diversify a greater portion of their funds, the research also shows it makes it more challenging for those funds to beat their respective benchmarks.

The Emergence of “Closet Indexing”

For decades, investors have sought to exploit market inefficiencies to achieve superior investment results. The poor performance of most actively managed mutual funds amid a healthy environment for global equity markets has fueled a major shift of investor flows from active to passive funds. The resulting reduction in assets, revenues and resources has contributed to an exodus of talent to more rewarding areas such as hedge funds, private equity funds or even non-financial sectors like technology. To mitigate the flight risk of their talent and in hopes of protecting their management fee revenue, many firms in the active management space have narrowed and restricted their investment mandates. Rather than seeking above benchmark performance, they instead seek to “be less bad than the others” and avoid termination by investment committees and consultants. As a result, more managers became “closet indexers.” It’s unsurprising that these managers’ performance outcomes have often disappointed due to this excess diversification and the low active share.5

Adding to the complexity of this analysis is that investment outperformance often begets growth in assets under management (AUM). Managers welcome the assets, as many are compensated on the assets they manage, not for outperformance. As successful active managers grow, it becomes more difficult to invest larger sums in a small number of portfolio holdings, particularly in smaller companies where there are greater pricing inefficiencies. As elucidated by Charles Ellis in his work, “The Rise and Fall of Performance Investing,” the sheer size of most large managers restricts their ability to operate concentrated portfolios, instead compelling them to invest primarily in a diversified group of the largest, most popular and most closely scrutinized stocks. We have long held a similar view that assets under management are the enemy of every good asset management firm, as larger asset bases necessitate increasing diversification that often dilutes performance of these once promising managers.

Similarly, the issue of closet indexing was highlighted in a recent whitepaper by Antti Petajisto, a former professor at the Yale School of Management. He evaluated this trend within the U.S. equity market and discovered that truly active investment managers, defined as those with an 80% or higher active share, plunged from over 60% of mutual fund managers in 1980 to less than 20% in 2009.6 In the same study, the average “stock picker,” defined as having an active share of more than 95%, was found to outperform their benchmark by 1.3% per year after taking out manager fees. All other segments, including the closet indexers and low-cost index funds, trailed their respective indices net of fees. Furthermore, the closet indexers, known for their benchmark-like performance and inflated effective management fees, typically underperformed the most.

On a related note, genuine active managers demonstrated superior capital protection especially during the 2008 market downturn and during the bursting of the tech bubble when this group was the only one to outperform their benchmark. This compelling evidence underscores the potential value and resilience of true active management despite the trend toward lower active share and closet index portfolios.

The Reaction of Investors

With the continued underperformance of traditional active managers, there has been a discernible shift towards low-cost, passive investments that are designed to replicate the return experience of their reference benchmark index. John Bogle, Vanguard’s founder and the innovator of index funds, famously advised, “Don’t look for the needle in the haystack. Just buy the haystack,” underscoring his support for low-cost and highly diversified solutions.7 He posited that investors are better off investing in a widely diversified portfolio, or in an entire market, rather than attempting to single out individual winners. A Morningstar report confirmed that in 2019, passive U.S. equity funds overtook their active counterparts in AUM for the first time, closing a $2 trillion gap over a 20-year period.8 This multi-decade trend indicates the reduced influence of active managers in the market.

Why don’t more investors seek out these true stock pickers with concentrated portfolios? First, the vast majority of active managers still cling to the old excessively diversified approaches. Further, the best of these managers are capacity constrained and don’t often offer their strategies on retail asset gathering structures such as mutual funds and separate account platforms found in the large banks and broker dealers. This makes identifying and accessing them difficult for the average investor. These managers are often among the largest investors in their own strategies, so performance rather than management fees matters most to them. This creates powerful alignment of interests with their investors, and they typically constrain capacity and the number of investors they allow into their strategies, making identifying and accessing them difficult for the average investor.

Making a Case for Concentrated Investing

While some may consider the approach of highly active, concentrated portfolios as being at the initial stages of a renaissance, concentrated investing is not new. It traces back to notable economist John Maynard Keynes who in 1934 advocated investing in a few carefully understood and trusted companies. Studies by renowned academics9 further endorse concentrated portfolios’ potential for outperformance, albeit with the very important caveat of needing superior stock-picking abilities.

With concentrated strategies, each security commands sufficient weight to significantly influence performance unlike those in highly diversified strategies where individual stock performance is largely lost in the sea of the market’s movements. A review of S&P 500 index performance starting in 2010 reveals that the annual top-performing stocks have consistently outpaced the “contributors” or those that most affect the index’s performance, a factor that takes into account both returns and weight of each security in the index. Despite the buzz around the returns of the largest companies the last couple of years, the average return of the top 10 performers has consistently eclipsed that of the top 10 contributors each year. This reiterates that, if executed proficiently, there are abundant opportunities to surpass the return of the index itself.

What Is the Right Number of Securities?

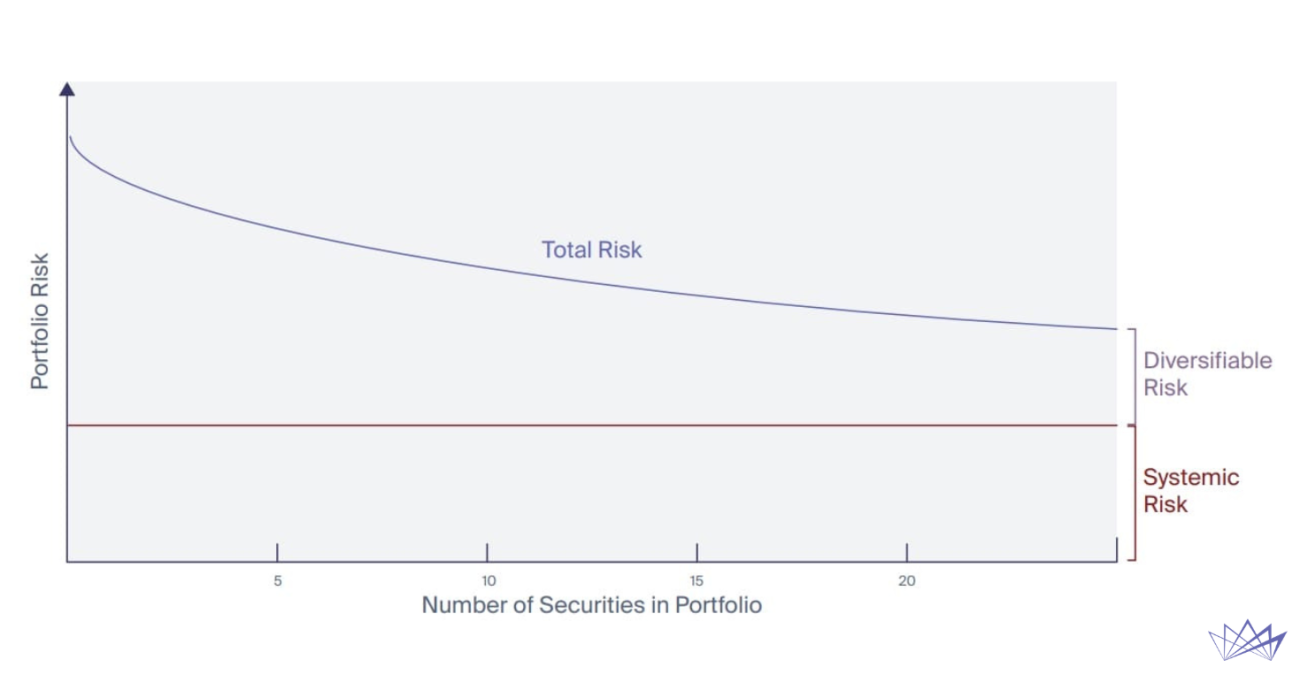

Striking the right balance between diversification to protect a portfolio and trying to generate alpha has been a topic of considerable debate among finance professionals. Burton Malkiel, in his iconic 1973 book, “A Random Walk Down Wall Street,” proposed that an ideal portfolio should contain around twenty securities. This concept as illustrated below shows how portfolio risk consistently decreases as the number of securities increases until reaching a point of plateau. This plateau represents non-diversifiable, systemic risk which is not reduced by further additions to the portfolio. This concept is widely accepted, but largely ignored by industry practitioners.

This exploration of optimal diversification started even before Malkiel’s milestone work with a seminal paper by John Evans and Stephen Archer in 1968 titled “Diversification and the Reduction of Dispersion: An Empirical Analysis,” where its authors suggested that as few as 15 stocks could achieve optimal diversification. A subsequent analysis in 2010, “Evans and Archer, 40 Years Later,” revisited this subject. This review revealed that most academics post-Evans and Archer have suggested the plateau of risk reduction is reached with a portfolio closer to 50 stocks, and in fact the 2010 paper presents a compelling argument that when risk is measured using standard deviation, full diversification is generally achieved with about 40 stocks.

Gresham’s Implementation of Concentrated Portfolios

While the emphasis in this article is on concentration, it is important to remember that we embrace diversification at a client’s overall portfolio level. However, we seek concentration any time we are pursuing individual actively managed strategies. Often, we recommend that clients build portfolios using a “core and satellite” framework, where the core of an equity portfolio might be a low cost passively managed index fund or, better still, a tax-managed index-tracking strategy where the underlying portfolios are lower-fee, widely diversified and highly liquid.

Gresham’s reputation for generating long-term performance rests on our ability to identify strategies across the global capital markets where active management is best suited for driving excess returns, and in turn identifying the best managers to implement those strategies. For these so-called alpha satellites, we must embrace concentration to generate better-than-benchmark performance. We agree with Warren Buffet that “very few people have gotten rich on their seventh best idea.” In building an alpha-seeking satellite strategy, such as our global equity partnership, we focus on underlying managers whose performance is driven by concentration, sometimes investing in only a handful of stocks. These managers endeavor to own misunderstood or mispriced companies with asymmetrical risk/reward dynamics, which are relatively rare. A deep understanding of the individual companies is necessary for this concentrated approach, which is more achievable when you own fewer companies.

The balance between core and satellites, or between diversified and concentrated exposures, should reflect a client’s individual preferences, goals and constraints. Our approach to portfolio construction was described in more detail in our paper “Gresham’s Refined Approach to Portfolio Construction and Improved After Tax Outcomes.”

Conclusion

The active management industry has become its own worst enemy by minimizing the art of risk-taking and concentration from their portfolios. The rise of passive investing can be directly linked to the ongoing and persistent underperformance of traditional active management. However, active management underperformance is not an investment truism, it is simply a reflection of current investment manager behavior. If this is the prevalent choice for most investors, this shift to passive, low-cost strategies shouldn’t surprise anyone. Fortunately, there is a better way, by simply returning to the golden age of active investing and embracing the idea that a concentrated portfolio of best ideas has a far stronger chance of outperforming broad market benchmarks.

We recognize that investing in concentrated portfolios for our actively managed, alpha-seeking strategies may lead to higher volatility and substantial deviation from short-term equity market performance. While enduring such volatility – and benchmark deviations – can be challenging, we believe this is an appropriate trade-off when pursuing performance. An investor can’t both track and beat a benchmark. There is room in a broad portfolio for both approaches, but investors must avoid landing in the muddled middle of the closet indexers who have become so prevalent.

Footnotes

1 Cremers, M., & Petajisto, A. (2009). How Active is Your Fund Manager? A New Measure That Predicts Performance. Review of Financial Studies.

2 Morningstar Direct. (2022). U.S. Active/Passive Barometer.

3 S&P Dow Jones Indices. (2023). S&P Indices Versus Active (SPIVA) Scorecard as of Dec 31, 2022.

4 Investment Company Institute and Morningstar. (2022). Investment Management Industry: Trends and Developments.

5 S&P Global Market Intelligence. (2023). Trends in Active and Passive Investments.

6 Petajisto, A. (2013). Active Share and Mutual Fund Performance. Financial Analysts Journal.

7 Bogle, J. (2007). The Little Book of Common Sense Investing. John Wiley & Sons.

8 Morningstar Direct. (2020). Fund Flows Report.

9 Petajisto, A. (2013). The Index Premium and its Hidden Cost for Index Funds. Journal of Empirical Finance; Kacperczyk, M., Sialm, C., & Zheng, L. (2005). On the Industry Concentration of Actively Managed Equity Mutual Funds. The Journal of Finance; Cohen, R., Polk, C., & Silli, B. (2010). Best Ideas. Harvard Business School.

The statements made in this article are the opinion of Gresham Partners and were developed from market research and data. Nothing in this article is intended to nor should be implied to be intended as any offer or solicitation for the purchase of securities or investments. No representation or warranty expressed or implied is made as to the accuracy or completeness of the information contained herein. Nothing contained herein should be relied upon as a promise or representation of future performance or as being intended to be investment advice.