What Is the Equity Risk Premium and Why It Matters Now?

By Ted Neild

History has shown that no one can time the markets or predict near-term returns, despite Wall Street analysts continuing to bombard us with their predictions. However, numerous studies have determined that current market prices or valuations do have an impact on future long-term returns. This won’t help us time markets, avoid crashes, or predict the S&P 500 return this year. But knowing where we are can help us improve our chance of long-term investment success. Understanding the Equity Risk Premium (“ERP”) can be helpful in this regard.

What Is It?

The Equity Risk Premium is a simple but powerful tool that provides a measure of relative market valuations. Specifically, it represents the expected extra return that investors demand for choosing the volatility of the stock market over the safety of risk-free assets like government bonds.

There are different ways to measure ERP, though they all share conceptual similarities. One simple approach is to compare the earnings yield (the inverse of the price/earnings multiple) of the S&P 500 Index with the yield on 10-year U.S. Treasuries. The former is a simple proxy for the broader stock market and the latter is a proxy for risk-free returns or high-quality bonds. When the earnings yield of equities is high relative to bond yields (high ERP), this signals equities are cheap and are likely to be relatively more appealing over the long term. Conversely, when the earnings yield for stocks is low relative to bond yields (low ERP), equities are relatively expensive and less attractive.

Where Are We Now?

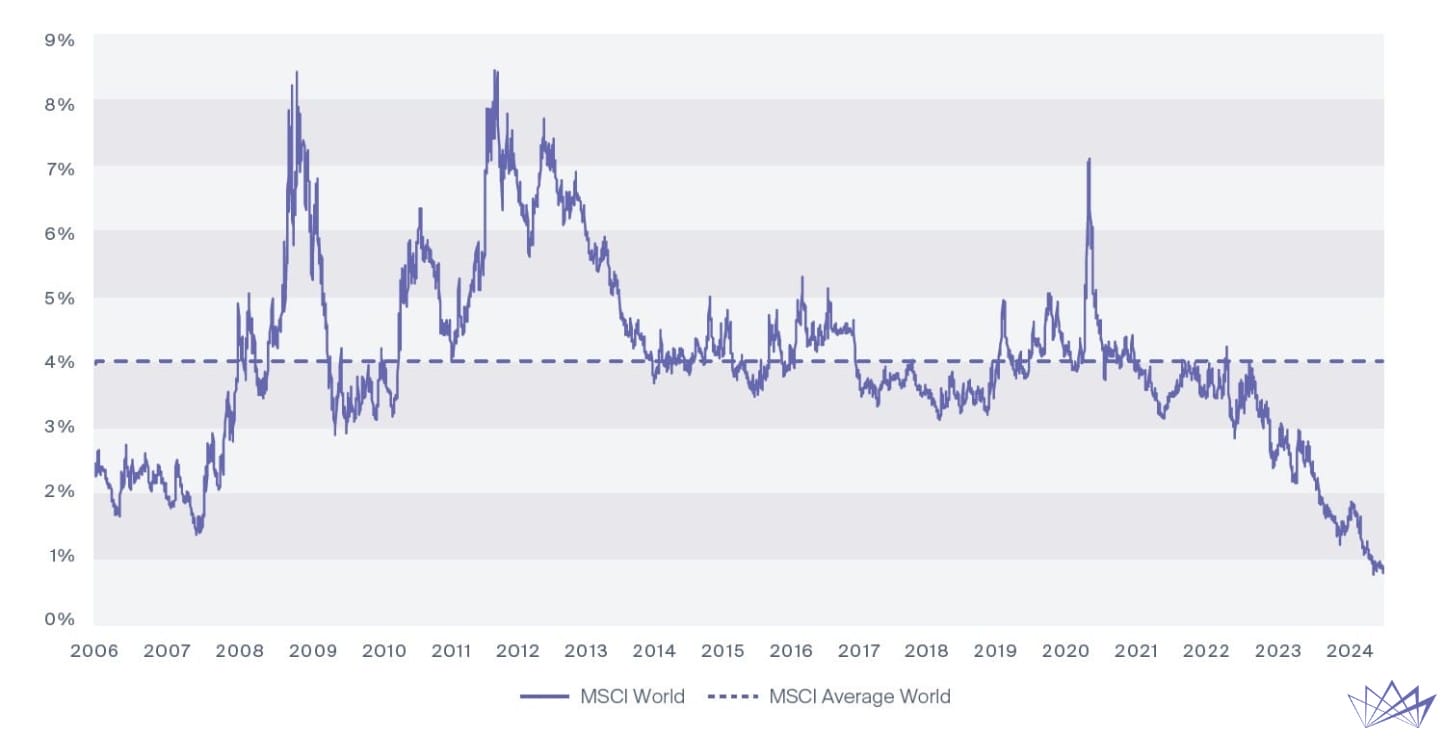

Due to a combination of strong recent equity market performance and increasing stock valuations alongside rising interest rates, ERP has been steadily declining and is nearing historically low levels not seen since prior to the Global Financial Crisis (see chart below). The low ERP indicates that bonds are becoming more attractive relative to stocks, just as the high ERP 15 years ago suggested that stocks were more compelling in the aftermath of the GFC.

What Should Investors Do?

Recognize that this is a rough cut using only the S&P 500 Index and the U.S. 10-year Treasury yield and is only one of many relative value indicators. And remember that the Equity Risk Premium cannot forecast how the stock market will perform in the short term. The ERP fluctuates every day and is at best a crude indicator for relative long-term return potential, not a tool for day trading.

However, today’s low ERP provides a general indication that equities have become more expensive while bonds have become relatively more attractive with implications for long-term investors. With that in mind, here are some other things to keep in mind:

- Do not time markets. It’s a loser’s game. While price has been shown to have an influence on long-term market returns, it has also been a horrible predictor of short-term market movements. There are no crystal balls and we are not (nor are we capable of) predicting a market crash.

- See #1 above.

- Rebalance. Aggressively. With recent market appreciation, most portfolios have become overweight relative to their long-term or strategic allocation targets. The risk of remaining overweight an overvalued asset class will eventually come back to bite us. I know it’s tempting to ride a winner, but don’t do it.

- Consider going further. Many investors’ portfolios have known cash needs such as spending, taxes, and capital calls to fund private investments. Typically, these expected annual outlays are measured in single digit percentage points (e.g., 4%) of the total investment portfolio. Consider raising a year of estimated outlays and simply holding it in cash or something similar. It may not seem like much, but it helps us to stay the course if the market declines and most importantly allows us to fund these outlays without selling equity assets after they have declined, locking in those losses.

- Don’t overdo it! It’s very possible – and even likely – that markets will muddle along and ERP will normalize. Making large, drastic changes away from your long-term strategic allocations can cause serious damage to your portfolio.

The statements made in this article are the opinion of Gresham Partners and were developed from market research and data. Nothing in this article is intended to nor should be implied to be intended as any offer or solicitation for the purchase of securities or investments. No representation or warranty expressed or implied is made as to the accuracy or completeness of the information contained herein. Nothing contained herein should be relied upon as a promise or representation of future performance or as being intended to be investment advice.